Kerala Plus Two Macroeconomics Notes Chapter 5 The Government: Budget and The Economy

Introduction

Three distinct functions of government.

- The allocation function: The government has to provide public goods such as national defense, roads, government administration. The public goods cannot be provided through the market mechanism.

- Distribution functions: The government affects the personal disposable income of households by making transfer payments and collecting taxes.

- Stabilization function: The government arrests the fluctuations in the economy by influencing the aggregate demand.

Public goods versus private goods

Public goods are those goods which one having two distinct features.

- Non-rivalry in consumption

- Non-excludability

Examples for public googs include nations defense, roads, government administrations etc.

Examples for private goods include clothes, cars, food items etc.

ആമുഖം

ഒരു ഗവൺമെന്റിന് മൂന്ന് സവിശേഷ ധർമ്മങ്ങളാണുള്ളത്.

a) വിഹിത ധർമ്മം: ദേശീയ പ്രതിരോധം, ഭരണം, റോഡുകൾ മുതലായ പൊതുവസ്തുക്കൾ (Public goods) നല്കേണ്ടത് ഗവൺമെന്റാണ്. ഉത്തരം പൊതുവസ്തുക്കൾ കമ്പോള സംവിധാനത്തിലുടെ നല്കാൻ സാധ്യമല്ല.

b) വിതരണധർമ്മം: കൈമാറ്റ അടവ് വഴിയും നികുതി ചുമ ത്തൽ വഴിയും ഗവൺമെന്റ് വ്യക്തിഗത വിനിമയ യോഗ്യമായ ഗാർഹിക വരുമാനത്തിൽ മാറ്റങ്ങൾ ഉണ്ടാക്കുന്നു.

c) സ്ഥിരതാ ധർമ്മം: സമ്പദ്വ്യവസ്ഥയിലെ വ്യതിയാനങ്ങളെ മൊത്ത ചോദനത്തിൽ മാറ്റം വരുത്തിക്കൊണ്ട് ഗവൺമെന്റ് സ്ഥിരതയിലേക്ക് നയിക്കുന്നു.

പൊതുവസ്തുക്കൾ/സ്വകാര്യ വസ്തുക്കൾ

താഴെ കൊടുത്തിരിക്കുന്ന രണ്ട് സവിശേഷതകളുള്ള വസ്തുക്ക ളാണ് പൊതുവസ്തുക്കൾ.

- ഉപഭോഗത്തിൽ പരസ്പരം മാത്സര്യമില്ലായ്മ.

- ഒഴിവാക്കാൻ സാധ്യമല്ലാത്തത്

ദേശീയ പ്രതിരോധം, ഗോഡ്, ഭരണം എന്നിവ പൊതുവസ്ത – ക്കൾക്ക് ഉദാഹരണമാണ്. വസ്ത്രങ്ങൾ, കാറുകൾ, ഭക്ഷ്യവസ്ത ക്കൾ എന്നിവ സ്വകാര്യ വസ്തുക്കൾക്കും ഉദാഹരണമാണ്.

Government Budget

The term budget is derived from the French word Bougette, meaning a small leather bag. It was used by then French finance minister to carry his financial statements. The annual financial statement with respect to the revenue and expenditure of the government is known as budget. The financial year of India starts from 1st April to 31st March. The annual financial statement is the main budget document. A budget statement shows the estimated expected income and expenditure of a financial year. In India, the budget is presented as per Article 112 of the Constitution. As per this Article, it is mandatory for the Government of India to present the estimated receipts and expenditure before the Parliament.

സർക്കാർ ബജറ്റ് (Government Budget)

ചെറിയ സഞ്ചി എന്നർത്ഥമുള്ള (Bougette) എന്ന ഫ്രഞ്ചു വാക്കിൽ നിന്നാണ് ബഡ്ജറ്റ് എന്ന പദം ഉണ്ടായത്. ധനകാര്യ നിർദ്ദേശങ്ങളടങ്ങുന്ന ഒരു സഞ്ചിയുടെ പ്രതിരൂപമാണ് ബഡ്ജറ്റ്. ഗവൺമെന്റിന്റെ ഒരു വർഷത്തിലെ (ഏപ്രിൽ 1 മുതൽ മാർച്ച് 31 വരെ) വരവിന്റെയും ചെലവിന്റെയും ഒരു മതിപ്പു കണക്കാണ് ബഡ്ജറ്റ്. അതായത്, അടുത്ത സാമ്പത്തിക വർഷത്തിലേക്ക് പ്രതീ ക്ഷിക്കുന്ന എല്ലാ വരവുകളുടേയും ചെലവുകളുടേയും എസ്റ്റി മേറ്റ് ഉൾക്കൊള്ളുന്ന വാർഷിക സാമ്പത്തിക രേഖയാണ് ബഡ്ജറ്റ്. ഒരു ബഡ്ജറ്റ്, പോയ വർഷത്തെ ധന അക്കൗണ്ടുകളും, തന്നാ ണ്ടത്തെ പുതുക്കിയ ബഡ്ജറ്റ് എസ്റ്റിമേറ്റുകളും, വരും വർഷത്തെ ബഡ്ജറ്റ് എസ്റ്റിമേറ്റുകളും കാണിക്കുന്നു.

ഒരു വാർഷിക ധനസ്റ്റേറ്റുമെന്റ് ലോകസഭയുടേയും രാജ്യസഭ യുടേയും മുന്നിൽ വച്ചിരിക്കണം എന്ന് ഇന്ത്യൻ ഭരണഘടയുടെ 112-ാം ആർട്ടിക്കിളിൽ നിർദ്ദേശിക്കുന്നു.

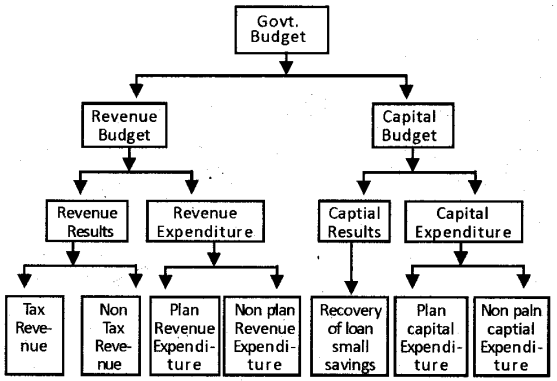

Components of Budget

Components fo govt. budget can be represented in the following chart.

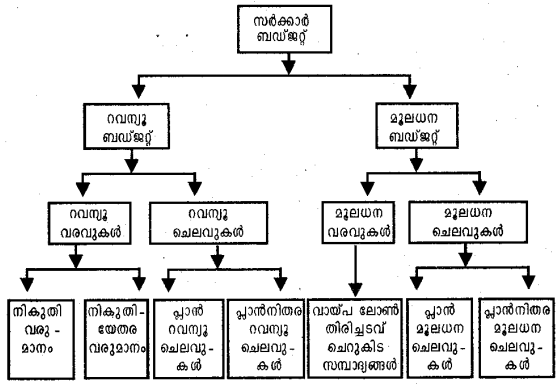

ബജറ്റിന്റെ ഘടകങ്ങൾ (Components of Budget)

സർക്കാർ ബജറ്റിന്റെ ഘടകങ്ങൾ ചുവടെ ചാർട്ടിൽ നൽകിയിരി ക്കുന്ന വിധം ക്രോഡീകരിക്കാം.

Components fo govt. budget can be represented in the following chart.

The Revenue Account

The Revenue Budget shows the current receipts of the government and the expenditure that can be met from these receipts.

Revenue Receipts: Revenue receipts are divided into tax and non-tax revenues. Tax revenues consist of the proceeds of taxes and other duties levied by the central government. Tax revenues, an important component of revenue receipts, comprise of direct taxes – which fall directly on individuals (personal income tax) and firms (corporation tax), and indirect taxes like excise taxes (duties levied on goods produced within the country), customs duties (taxes imposed on goods imported into and exported out of India) and service tax.

Revenue Expenditure: Broadly speaking, revenue expenditure consists of all those expenditures of the government which do not result in creation of physical or financial assets. It relates to those expenses incurred for the normal functioning of the government departments and various services, interest payments on debt incurred by the government, and grants given to state governments and other parties.

റവന്യ ബജറ്റ്: ഗവൺമെന്റിന്റെ റവന്യൂ വരവുകളും റവന്യ ചെലവുകളും ചേർന്നതാണ് റവന്യ ബജറ്റ്.

റവനു വരവ്: ഗവൺമെന്റിന്റെ ആസ്തി വർദ്ധിപ്പിക്കുന്ന വര വുകളാണ് റവന്യൂ വരവുകൾ. ഇതിൽ നികുതി വരുമാനവും നികുതിയേതര വരുമാനവും ഉൾപ്പെടും. പ്രത്യക്ഷ നികുതിയും പരോക്ഷ നികുതിയും അടങ്ങുന്നതാണ് നികുതി വരുമാനം.

റവന്യ ചെലവുകൾ: ഗവൺമെന്റിന്റെ ദൈനംദിന പ്രവർത്തന ങ്ങൾക്കുള്ള ചെലവാണ് റവന്യൂ ചെലവ്. വിവിധ ഗവൺമെന്റ് വകുപ്പുകളുടെ പ്രവർത്തനത്തിനും പലിശ അടവ്, ഗ്രാന്റുകൾ, സബ്സിഡികൾ, ദുരിതാശ്വാസം, ദേശരക്ഷ തുടങ്ങിയ ഗവൺ മെന്റ് സേവനങ്ങൾക്കും വേണ്ടി വരുന്ന ചെലവാണിത്. ഇവ ഗവൺമെന്റിന്റെ ബാധ്യതകൾ കുറയ്ക്കുകയോ ആസ്തികൾ സൃഷ്ടിക്കുകയോ ചെയ്യുന്നവയല്ല. റവന ചെലവുകളെ രണ്ടായി തിരിക്കാം. പദ്ധതി റവന്യൂ ചെല വുകളും (Plan Revenue expenditure) പദ്ധതിയേതര റവന്യ ചെലവുകളും (Non-plan revenue expenditure).

The Capital Account

The Capital Budget is an account of the assets as well as liabilities of the central government, which takes into consideration changes in capital. It consists of capital receipts and capital expenditure of the government. This shows the capital requirements of the government and the pattern of their financing.

Capital Receipts: The main items of capital receipts are loans raised by the government from the public which are called market borrowings, borrowing by the government from the Reserve Bank and commercial banks and other financial institutions through the sale of treasury bills, loans received from foreign governments and international organizations, and recoveries of loans granted by the central government. Other items include small savings (PostOffice Savings Accounts, National Savings Certificates, etc), provident funds and net receipts obtained from the sale of shares in Public Sector Undertakings (PSUs).

Capital Expenditure: This includes expenditure on the acquisition of land, building, machinery, and equipment, investment in shares, and loans and advances by the central government to state and union territory governments, PSUs and other parties. Capital expenditure is also categorized as plan and non-plan in the budget documents.

മൂലധന ബഡ്ജറ്റ്: മൂലധന ബഡ്ജറ്റ് ഗവൺമെന്റിന്റെ ആസ്തി യുടേയും ബാധ്യതയുടേയും അക്കൗണ്ടാണ് മൂലധനവരവുകളും മൂലധന ചെലവുകളും ചേർന്നതാണ് മൂലധന ബഡ്ജറ്റ്.

i) മൂലധന വരവുകൾ: ഗവൺമെന്റിന്റെ ആസ്തികൾ ക്ഷയിപ്പി . ക്കുകയോ ബാധ്യതകൾ ഉണ്ടാക്കുകയോ ചെയ്യുന്ന വരുമാ നത്ത മൂലധന വരവുകൾ എന്നു പറയുന്നു. പൊതുജന ങ്ങളിൽനിന്നും ഗവൺമെന്റ് സ്വീകരിക്കുന്ന വായ്പകൾ, ട്രഷറി ബില്ലുകളുടെ വില്പനയിലൂടെ കേന്ദ്, വാണിജ്യ ബാങ്കുകളിൽ നിന്നും മറ്റ് ധനകാര്യ സ്ഥാപനങ്ങളിൽ നിന്നും വാങ്ങുന്ന വായ്പ വിദേശ ഗവൺമെന്റുകളിൽ നിന്നും അന്താരാഷ്ട്ര സംഘടനകളിൽ നിന്നും വാങ്ങുന്ന വായ്പകൾ, എൻ.എസ്.സി. പോലെയുള്ള ചെറുകിട സമ്പാദ്യങ്ങൾ, പി. എഫ്, പൊതുമേഖലാ സ്ഥാപനങ്ങളുടെ ഓഹരികൾ വിറ്റഴി ക്കലിലൂടെ ലഭിക്കുന്ന വരുമാനം മുതലായവ ഇതിൽപെടും.

ii) മൂലധന ചെലവുകൾ: ഭൗതികമോ സാമ്പത്തികമോ ആയ ആസ്തികൾ സൃഷ്ടിക്കുകയോ ഗവൺമെന്റിന് ബാധ്യതകൾ കുറയ്ക്കുകയോ ചെയ്യുന്ന ഗവൺമെന്റ് ചെലവുകളാണ് മൂലധന ചെലവുകൾ. ഓഹരികളിന്മേലുള്ള നിക്ഷേപം, സംസ്ഥാനങ്ങൾക്കും കേന്ദ്ര ഭരണപ്രദേശങ്ങൾക്കും വിദേ ശരാജ്യങ്ങൾക്കുമുള്ള വായ്പകൾ, പൊതുമേഖലാസ്ഥാപന ങ്ങൾക്കുള്ള വായ്പകൾ, ദേശരക്ഷയ്ക്കുവേണ്ടിയുള്ള ചെല വുകൾ മുതലായവ ഇതിൽപ്പെടും.

മൂലധന ചെലവുകളെ പദ്ധതി മൂലധന ചെലവുകൾ, പദ്ധ തിയേതര മൂലധന ചെലവുകൾ എന്നിങ്ങനെ രണ്ടായി തിരിക്കാം.

Types of Budget

The budget can be classified into balanced budget and unbalanced budget. When the revenue and the expenditures of the governments become equal, it is the case of balanced budget. When government expenditure is not equal to its reveue, it is the case of unbalanced budget. Unbalanced budget can be of deficit budget or surplus budget.

വിവിധതരം ബജറ്റുകൾ

ഒരു നിശ്ചിത വർഷത്തെ പല ഹെഡുകളിലുള്ള വരവുകളു ടെയും ചെലവുകളുടെയും ഇനം തിരിച്ചുള്ള എസ്റ്റിമേറ്റ് അവത രിപ്പിക്കുന്ന വാർഷിക സ്റ്റേറ്റ്മെന്റാണ് ഗവൺമെന്റ് ബഡ്ജറ്റ്. ബഡ് ജറ്റ് സന്തുലിതമോ, അസന്തുലിതമോ ആകാം. അസുലിതമായ ബഡ്ജറ്റ് മിച്ചമോ കമ്മിയോ ആകാം. വരവ് ചെലവുമായി തുല്യമാ യാൽ അതിനെ സന്തുലിത ബഡ്ജറ്റ് എന്നു പറയും. വരവ് ചെല വിനേക്കാൾ കുറവായിരുന്നാൽ കമ്മി ബഡ്ജറ്റ് എന്നും വരവ് ചെലവിനേക്കാൾ കൂടിയിരുന്നാൽ മിച്ച് ബഡ്ജറ്റ് എന്നു പറയും.

Measures of Government Deficit

When a government spends more than it collects by way of revenue, it incurs a budget deficit. There are various measures that capture government deficit and they have their own implications for the economy.

Revenue Deficit: The revenue deficit refers to the excess of government’s revenue expenditure over revenue receipts

Revenue deficit = Revenue expenditure – Revenue receipts

Fiscal Deficit: Fiscal deficit is the difference between the government’s total expenditure and its total receipts excluding borrowing.

Gross fiscal deficit = Total expenditure – (Revenue receipts + Non-debt creating capital receipts

Primary Deficit: We must note that the borrowing requirement of the government includes interest obligations on accumulated debt. To obtain an estimate of borrowing on account of current expenditures exceeding revenues, we need to calculate what has been called the primary deficit. It is simply the fiscal deficit minus the interest payments.

Gross primary deficit = Gross fiscal deficit – net interest liabilities.

ഗവൺമെന്റ് ബജറ്റ് കമ്മിയുടെ അളവുകൾ (Measures of Govt.deficit)

വിവിധ തരം ബജറ്റ് കമ്മികൾ ചുവടെ തന്നിരിക്കുന്നു.

ബഡ്ജറ്റ് കമ്മി (Budget deficit): മൊത്തം ചെലവിൽ നിന്ന്, വർത്തമാനകാല വരവുകളും അറ്റ് ആഭ്യന്തര ബാഹ്യമൂലധന വരവുകളും ചേർത്ത് കുറച്ചുകിട്ടുന്ന സംഖ്യയാണ് ബഡ്ജറ്റ് കമ്മി. അറ്റ ആഭ്യന്തര, ബാഹ്യ മൂലധനവരവുകളിൽ നിന്നാണ് ഈ കമ്മി നികത്തുന്നത്. ഇന്ത്യയുടെ യുണിയൻ ബഡ്ജറ്റിൽ ഈ ഇനം പ്രത്യേകിച്ച് രേഖപ്പെടുത്താറില്ല.

ബഡ്ജറ്റ് കമ്മി = മൊച്ചെ ചെലവ് – മൊത്തം വരുമാനം

i) റവന്യൂ കമ്മി (Revenue deficit): ഗവൺമെന്റിന്റെ റവന ചെലവിൽ നിന്ന് റവന്യൂ വരവ് കുറച്ചുകിട്ടുന്ന സംഖ്യ – യാണിത്. ഗവൺമെന്റിന്റെ നിലവിലുള്ള റവന്യൂ വരുമാനം (നികുതി, നികുതിയേതര വരുമാനങ്ങൾ) നിലവിലുള്ള ചെലവിന് തികയില്ല എന്നാണ് ഇതിന്റെ അർത്ഥം. ഈ കമ്മി നികത്തുന്നതിന്, ഗവൺമെന്റ് കടം എടുക്കുകയോ മുത ലിറക്കാതെ പണം സ്വരൂപിക്കുകയോ ചെയ്യണം.

റവന്യൂ കമ്മി = റവനു ചെലവ് – റവന്യൂ വരുമാനം

ii) ധന കമ്മി (Fiscal deficit): ഗവൺമെന്റിന്റെ മൊത്തം ചെലവും, വായ്പയൊഴികെയുള്ള മൊത്തം വരുമാനവും തമ്മിലുള്ള വ്യത്യാസമാണ് ധനകമ്മി.

മൊത്ത ചെലവ് എന്നതിൽ വർത്തമാന ചെലവും മൂലധന ചെലവും ഉൾപ്പെടുന്നു. ആഭ്യന്തര അഥവാ ബാഹ്യ ഉറവിട ങ്ങളിൽ നിന്നും കടം എടുത്തോ, കേന്ദ്ര ബാങ്കിൽ നിന്നോ കടം എടുത്തോ, രണ്ടും കൂടി ഉപയോഗിച്ചോ ആണ് ധനകമ്മി നികത്തുന്നത്.

ധനകമ്മി = ആകെ ചെലവ്- വായ്പയൊഴികെയുള്ള വരുമാനം

iii) പ്രാഥമിക കമ്മി: ധനകമ്മിയിൽ നിന്ന് പലിശ ഇനത്തിലുള്ള അടവുകൾ കുറച്ചാൽ കിട്ടുന്ന സംഖ്യയാണിത്.

പ്രാഥമിക കമ്മി = ധനകമ്മി – പലിശ അടവുകൾ

Fiscal Policy

One of Keynes’s main ideas in ‘The General Theory of Employment, Interest and Money’ was that government fiscal policy should be used to stabilize the level of output and employment. Through changes in its expenditure and taxes, the government attempts to increase output and income and seeks to stabilize ups and downs in the economy. In the process, fiscal policy creates a surplus (when total receipts exceed expenditure) or a deficit budget (when total expenditure exceeds receipts) rather than a balanced budget (when expenditure equals receipts). In what follows, we study the effects of introducing the government sector in our earlier analysis of the determination of income.

ഫിക്സൽ നയം

പൊതു ചെലവുകൾ, നികുതി ചുമത്തൽ, കടംവാങ്ങൽ എന്നി വയെ സംബന്ധിച്ചുള്ള ഗവൺമെന്റിന്റെ നയത്തെ ഫിസൽ നയം എന്നു പറയുന്നു. ജെ.എം. കെയ്ൻസ് ആണ് ഫിസ്കൽ നയം പ്രസിദ്ധമാക്കിയത്. സമ്പദ്വ്യവസ്ഥ അസ്ഥിരമാകുമ്പോൾ അതിനെ സ്ഥിരപ്പെടുത്താൻ സർക്കാർ നടപ്പാക്കുന്ന നയ ങ്ങളാണ് ഫിസ്കൽ നയം. അധിക- നനചോദനങ്ങൾ ഉചിത മായ ഫിസ്കൽ നയങ്ങളിലൂടെ പരിഹരിക്കാവുന്നതാണ്.

നികുതി ചുമത്തൽ (T) ഗവൺമെന്റ് ചെലവുകൾ (G) എന്നീ ഫിസ്കൽ നടപടികളിലൂടെ ഗവൺമെന്റുകൾക്ക് സമ്പദ്വ്യവ സ്ഥയിൽ ഇടപെടാനും അതിനെ സ്ഥിരപ്പെടുത്താനും കഴിയും.

Fiscal Responsibility and Budget Management Act, 2003 (FRBMA)

In a multiparty parliamentary system, electoral concems play an important role in determining expenditure policies. A legislative provision, it is argued, that is applicable to all governments – present and future – is likely to be effective in keeping deficits under control. The enactment of the FRBMA, in August 2003, marked a turning point in fiscal reforms, binding the government through an institutional framework to pursue a prudent fiscal policy, The central government must ensure inter-generational equity, long-term macroeconomic stability by achieving sufficient revenue surplus, removing fiscal obstacles to monetary policy and effective debt management by limiting deficits and borrowing. The rules under the Act were notified with effect from July, 2004. ഫി

ക്സൽ റെസ്പോൺസിബിലിറ്റി ആന്റ് മാനേജ്മെന്റ് ആക്ട് – (FREMA) – 2003

സാമ്പത്തിക അച്ചടക്കം പാലിക്കുവാൻ ഗവൺമെന്റിനെ നിർ ബന്ധിക്കുന്ന ഒരു നയരേഖയാണ് FRBMA, കേന്ദ്ര – സംസ്ഥാന ഗവൺമെന്റുകളെ സാമ്പത്തിക അച്ചടക്കം പാലിക്കുവാൻ നിർ ബന്ധിതരാക്കുക എന്നതാണ് ഈ നിയമത്തിന്റെ ലക്ഷ്യം. ഈ നിയമത്തിന്റെ പ്രധാന ആശയങ്ങൾ ഇവയാണ്.

1. ഫിസ്കൽ കമ്മിയും റവന്യൂ കമ്മിയും കുറയ്ക്കുന്നതിന് ഈ നിയമം ഗവൺമെന്റിന് അധികാരം നൽകുന്നു. ഫിസ്കൾ കമ്മി GDP യുടെ 3% ത്തിൽ താഴെയായി നിർത്തണം 2009 മാർച്ചോടു കൂടി റവന്യൂ കമ്മി ഇല്ലാതാക്കാനും ഈ നിയമം വ്യവസ്ഥ ചെയ്യുന്നു.

2. ഓരോ വർഷവും ഫിസൽ കമ്മി GDP യുടെ 3% വീതവും റവന്യൂ കമ്മി GDP യുടെ 5% വീതവും കുറയ്ക്കണം . ഇത് നികുതി വരുമാനത്തിലെ വർദ്ധനവുകൊണ്ട് നേടാൻ കഴിയുന്നില്ലെങ്കിൽ ചെലവു കുറച്ചുകൊണ്ട് നേടണം.

3. പ്രകൃതിക്ഷോഭങ്ങൾ, രാജ്യരക്ഷയുമായി ബന്ധപ്പെട്ട സാഹ ചര്യങ്ങൾ തുടങ്ങി അടിയന്തിര സാഹചര്യങ്ങളിൽ മാത്രമേ മുൻകൂട്ടി നിശ്ചയിച്ച ലക്ഷ്യങ്ങളിൽ നിന്ന് വ്യതിചലിക്കാവൂ.

4. RBI യിൽ നിന്നും കേന്ദ്ര സർക്കാർ അഡ്വാൻസ് ആയി മാത്രമേ കടം വാങ്ങാവു.

5. ധന നടപടികളിൽ കൂടുതൽ സുതാര്യത പുലർത്തുക.

6. കേന്ദ്ര ഗവൺമെന്റ് പാർലമെന്റിനു മുമ്പിൽ മൂന്നു രേഖകൾ സമർപ്പിക്കണം.

- ഇടക്കാല ഫിസ്കൽ നയതന്ത്രരേഖ

- ഫിസ്കൽ നയത്രന്തരേഖ

- വാർഷിക സാമ്പത്തിക രേഖ എന്നിവ.

7. മൂന്നുമാസം കൂടുമ്പോൾ പാർലമെന്റിനു മുമ്പാകെ വരു മാനത്തിലെയും ചെലവിലെയും മാറ്റങ്ങൾ അവതരിപ്പി ക്കണം. കേന്ദ്ര-സംസ്ഥാന ഗവൺമെന്റുകളെ സാമ്പത്തിക അച്ചടക്കം പാലിക്കുവാൻ നിർബന്ധിപ്പിക്കുക എന്നതാണ് ഈ നിയമത്തിന്റെ ലക്ഷ്യം.